Coronavirus Relief Fund: Updates to the CARES Act

April 3, 2020 |

Written by: Katherine Holmok, PLA, ASLA

The success of business, municipalities and non-profits is paramount to the future of our families, communities and mission. As such, we want to share an overview of the Federal Coronavirus Aid, Relief, and Economic Security Act (CARES) and how it can help. The CARES Act provides more than $2 trillion in relief and makes economic support available to midsize and large businesses, including non-profits and state and local governments. Here’s how:

Nonprofits

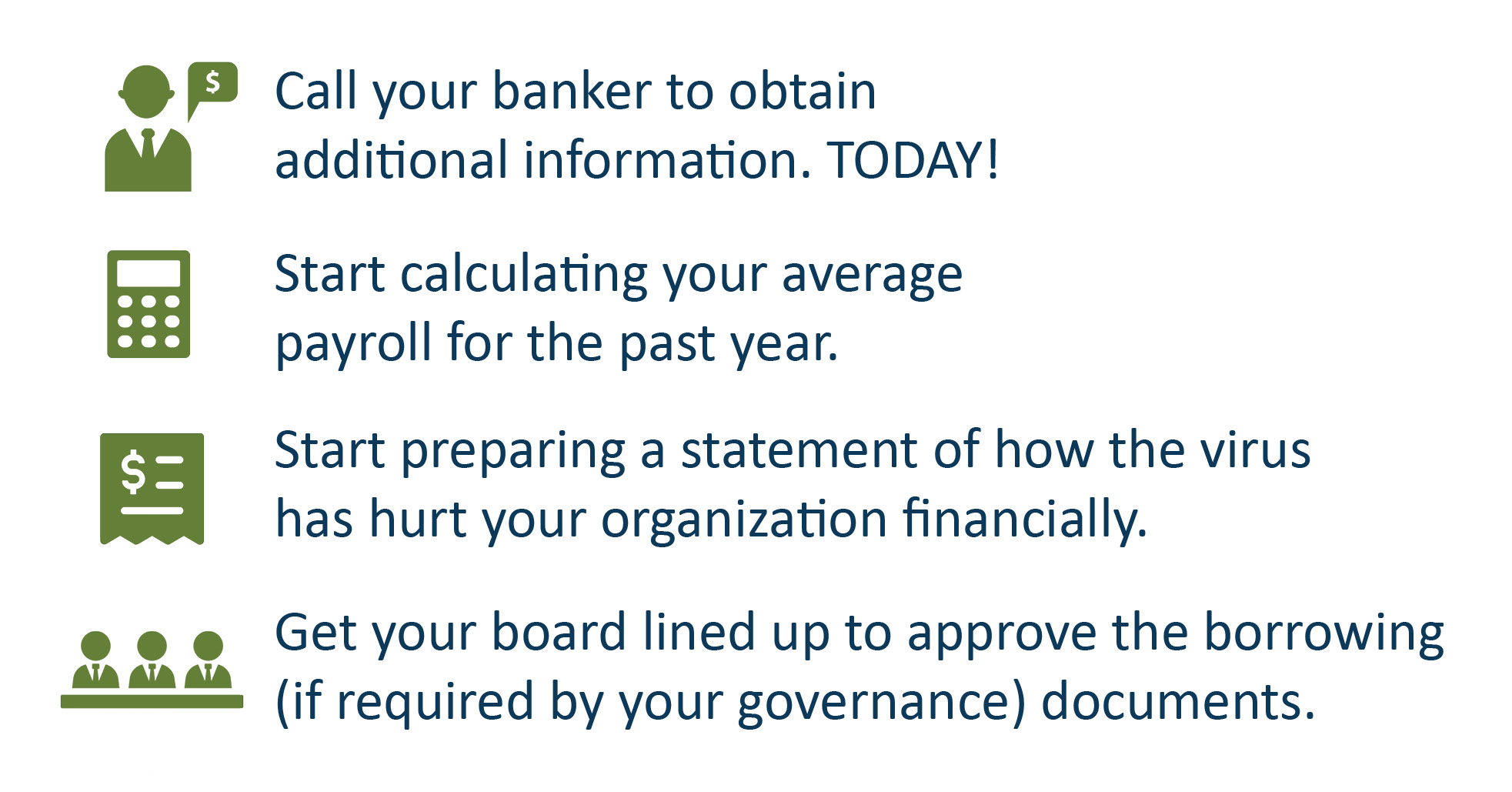

- Paycheck Protection Program Loans: The Small Business Association (SBA) has opened the ability to apply for an emergency loan/grant for small businesses and non-profits. This is what you need to do:

Loan amounts will be 2.5 times the average total monthly payroll costs from the prior year. These funds can be used to make payroll and associated costs, including health and retirement benefits, facilities costs, and debt service. Employers that maintain employment for the eight weeks after the origination of the loan, or rehire employees by June 30, would be eligible to have their loans forgiven (essentially turning the loan into a grant).

2. Economic Injury Disaster Loans

2. Economic Injury Disaster Loans

The disaster loan program creates emergency grants for eligible nonprofits and other applicants with 500 or fewer employees, enabling them to receive a check for $10,000 within three days (Section 1110). You can view the application here.

3. Self-funded Nonprofits and Unemployment

Self-funded nonprofits can be reimbursed for half of the cost of benefits provided to their laid-off employees.

4. Charitable Giving Incentive

The charitable giving incentive included in the CARES Act creates a new above-the-line deduction (universal or non-itemizer deduction that applies to all taxpayers) for total charitable contributions of up to $300. The incentive applies to cash contributions made in 2020 and can be claimed on tax forms next year (Section 2204). The law also lifts the existing cap on annual contributions for those who itemize, raising it from 60 percent of adjusted gross income to 100 percent. For corporations, the law raises the annual limit from 10 percent to 25 percent (Section 2205).

State and Local Entities

In total, states and municipalities will receive $150 billion. Reserved within that amount is $8 billion for Indian Tribes and $3 billion for DC and U.S. Territories. Funds are allocated proportionally based on state population. No state that is one of the 50 states will receive less than $1.25 billion.

To calculate the amount for a state:

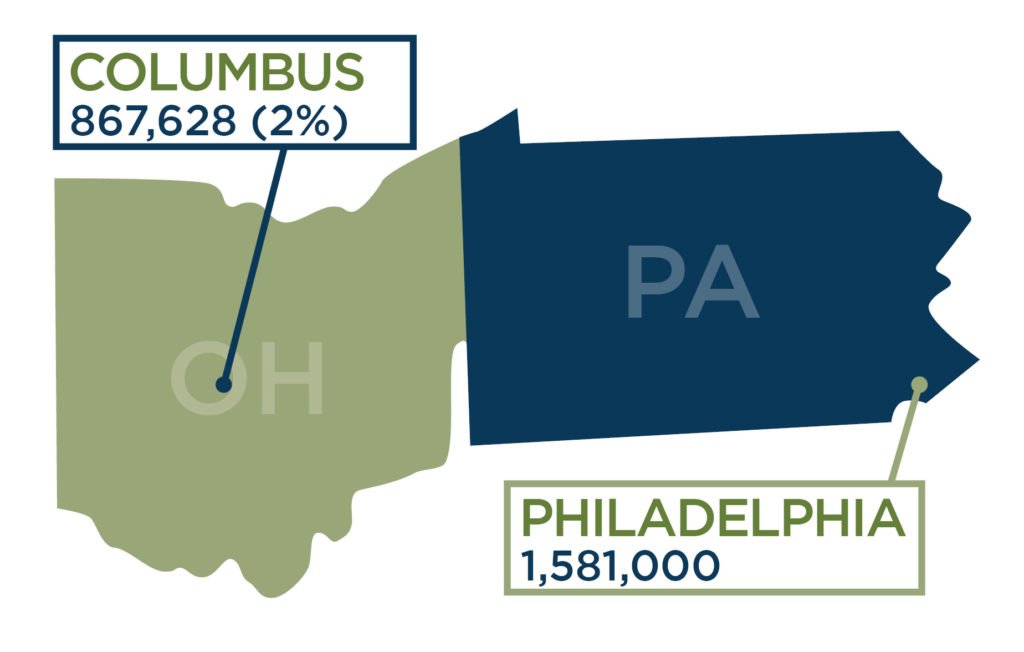

Only municipalities larger than 500,000 in population can apply directly to the federal government for their relative share by population. Those requested dollars will come out of that municipality’s state allocation (i.e. Columbus’s request to the federal government will come out of the State of Ohio’s allocation). Those larger municipalities can request a calculation of [the municipalities population/state population] up to 45% of the state’s allocated amount.

The only municipality in Ohio above 500,000 is Columbus. The only municipality in Pennsylvania is Philadelphia. Ohio will receive $4,533,000,000 (minus Columbus request) and Pennsylvania will receive $4,964,000,000 (minus Philadelphia request).

The state shall make available 45% of its state share to these entities. How this money is requested or given out from each state, was not identified in the federal bill. That information will probably be determined by each state governor.

The Treasury will automatically award each state its share within 30 days. Qualifying localities (Columbus and Philadelphia), however, must apply to Treasury to access their share of state funds. This funding is available directly to states and localities from Treasury and requires no state or local matching requirement. Details on how Ohio and Pennsylvania’s allocation will be used is not yet known.

What can the allocated funding be used for?

The allocated funding can be used for necessary expenditures incurred due to the COVID-19 public health emergency or state and local expenditures not accounted for in the most recent approved budget. This only applies to expenditures incurred between March 1 and December 30, 2020. This funding is not revenue replacement funding.

As we continue discovering information, we will share it appropriately. Thank you and stay safe!

RELATED INSIGHTS:

RELATED TAGS:

[xyz-ips snippet=”comment-form”]